Palantir's CEO on AI Pricing: What It Means for TaxTech

Alex Karp says token-based AI pricing is broken. Here's how his CNBC remarks connect to TaxTech vendor pricing and AI value measurement.

On July 1, Palantir CEO Alex Karp joined CNBC's Squawk Box to discuss the company's expanded Nvidia partnership — folding Nvidia's Nemotron models into Palantir's Sovereign AI platform so enterprises and governments can run AI while retaining control of their data and model weights.

Partway through, he turned to how the rest of the industry prices AI: “I’m not throwing shade at them, but something has gone completely wrong” with the token-based model used by OpenAI and Anthropic. On enterprise buyers specifically: “The basic view among enterprises in this country is I’m going to chillax and waste my time with tokens.”

In a follow-up interview with The Information, published the same week, Karp framed the issue less as pricing and more as competitive exposure: “There’s just very deep frustration around…are they gonna optimize the models for me, or are they gonna take the alpha of my business, transfer in their weights, and compete against me?”

Worth noting for balance: I’ve found no evidence that Anthropic or OpenAI train on enterprise customer data, but they are likely tracking domain usage, customer personas, prompts, and other metadata.

Karp’s “alpha” framing is a claim about risk exposure, not a documented incident — and it doubles as the pitch for Palantir’s own position as the “application layer” sitting between enterprise data and whichever model a customer chooses. It’s a competitive stance as much as a pricing critique, and both readings are worth holding at once.

I’m not in a position to referee any of this. What I noticed is that several of the points mentioned in the interview touch things I’ve written about this year.

On Measuring Value Instead of Usage

Two months ago, Amazon retired its internal AI leaderboard after employees optimized for token volume rather than useful output. I wrote about why usage is the wrong metric to track at the time — Amazon’s replacement metric counted deployments that actually shipped, not activity. Karp’s comment about enterprises “wasting time with tokens” is describing the same gap between activity and value, from the vendor side rather than the buyer side.

On Vendor Transparency

Separately, I’ve argued that TaxTech AI vendors should carry the same SLA discipline enterprises already require from AWS — visibility into which model handles a given request, at what cost. Palantir’s own answer to that question happens to be a product feature: Evolve, which the company describes as including a “model router” that sends a given task to different models depending on whether the customer is optimizing for performance or cost. Whatever one makes of the business strategy behind it, a router that surfaces model selection and cost is closer to the infrastructure layer I described than most TaxTech vendors currently offer.

Karp also drew a sharper line between American and Chinese open-source models — “the choice is going to be very quickly [an] open model from America or open model from China”. That’s not just a model-selection debate for AI labs. It’s a version of the same data-residency question TaxTech vendors already navigate under GDPR, e-invoicing mandates, and cross-border VAT rules, with model origin as a new variable.

On the Stakes for Finance Specifically

I’m finishing a longer piece for next week on why finance and tax now make up the single largest category in Anthropic’s own Claude Connectors directory — 57 of 439 connectors, ahead of coding and marketing. Full breakdown and sourcing coming in that post. The early number is enough to make the point here: unsettled model-vendor economics flow directly into the tools running reconciliation, VAT determination, and transfer pricing documentation. More on this next week.

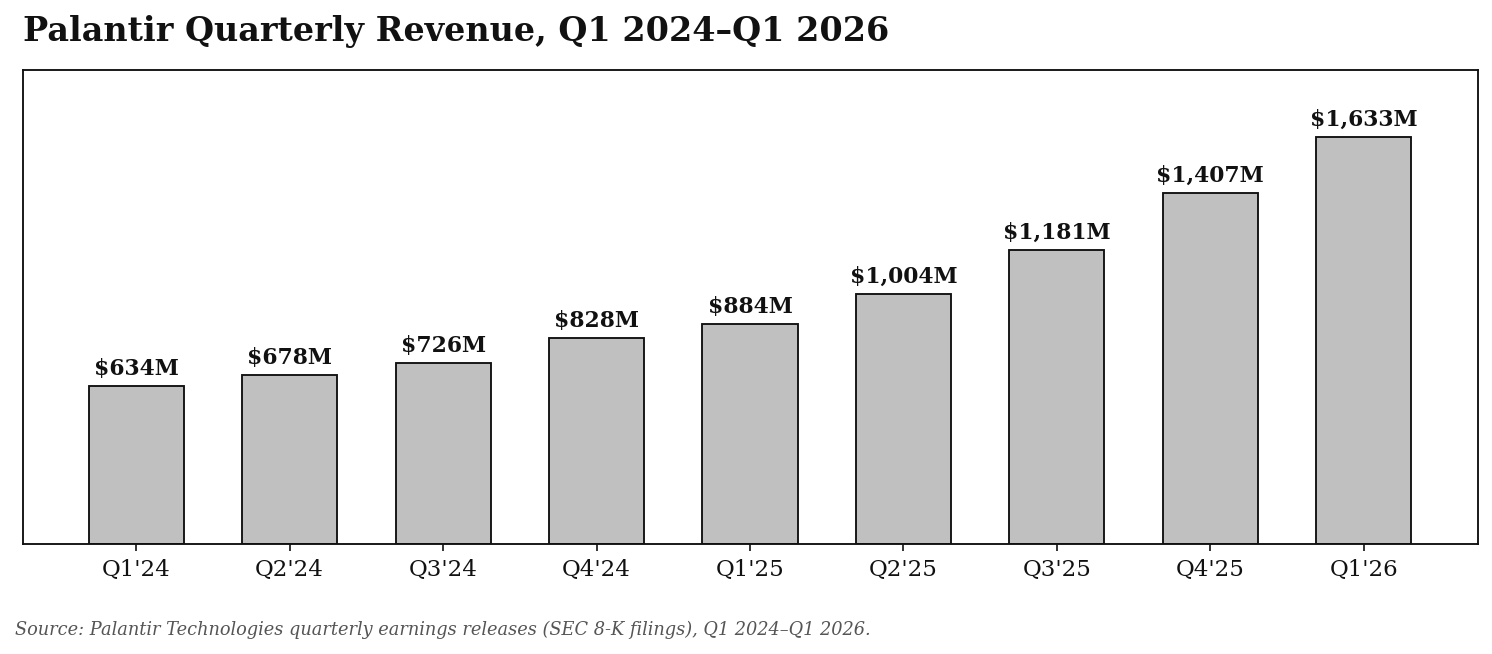

What Palantir’s Own Numbers Show

Whatever one makes of the positioning, Karp’s company has a multi-year track record worth putting next to the comments. Palantir’s quarterly revenue has climbed for nine straight quarters:

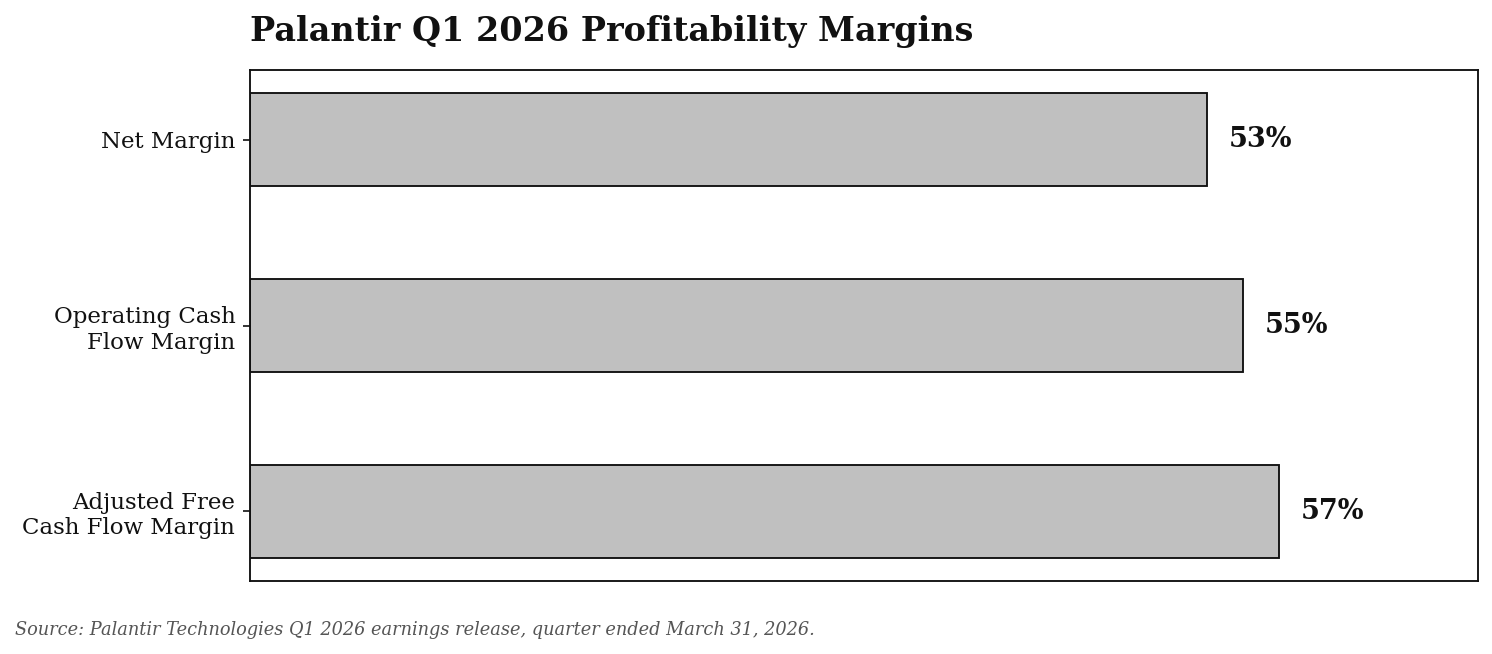

In Q1 2026 specifically, Palantir reported revenue of $1.63B, up 85% year over year, with net income of $870.5M. Cash generation moved in step with revenue:

A 53% net margin, a 55% operating cash flow margin, and a 57% adjusted free cash flow margin, against $8B in cash and short-term treasuries on the balance sheet. Palantir raised full-year 2026 guidance to $7.65–7.66B in revenue (roughly 71% growth), with a Rule of 40 score of 145%. Palantir’s commercial model has leaned on enterprise platform and outcome-based contracts (Foundry, AIP, Evolve) rather than pure per-token API pricing — one way to read why its CEO frames token metering as the wrong model for building a durable enterprise business.

Worth watching as more TaxTech and finance AI tools move to usage-based pricing: whether buyers get the model-level transparency Karp says Palantir’s router provides, or stay inside the token-metered model he’s pushing back on.

🔮 Strategic Forecast: By the end of 2027, expect at least one major TaxTech vendor to publicly shift part of its AI pricing from pure token/usage metering toward outcome- or platform-based tiers, citing enterprise buyer feedback as the reason.

References & Further Reading

CNBC — “Palantir CEO Alex Karp says ‘something has gone completely wrong’ with how AI is sold” — https://www.cnbc.com/video/2026/07/01/palantir-ceo-alex-karp-says-something-has-gone-completely-wrong-with-how-ai-is-sold.html — Accessed 2026-07-03

CNBC — “Palantir’s Karp bashes OpenAI, Anthropic token model: ‘Something has gone completely wrong’” — https://www.cnbc.com/2026/07/01/palantir-karp-open-ai-anthropic-tokens.html — Accessed 2026-07-03

The Information (Laura Bratton, Applied AI) — “Palantir CEO Says Some U.S. Government Customers Switched to Open Source AI” — https://www.theinformation.com/newsletters/applied-ai/palantir-ceo-says-u-s-government-customers-switched-open-source-ai — Accessed 2026-07-03

Palantir Technologies — Q1 2026 Earnings Release / Investor Relations — https://investors.palantir.com/news-details/2026/Palantir-Reports-Q1-2026-U-S--Revenue-Growth-of-104-YY-and-Revenue-Growth-of-85-YY-Raises-FY-2026-Revenue-Guidance-to-71-YY-Growth-and-U-S--Comm-Revenue-Guidance-to-120-YY-Crushing-Consensus-Expectations/ — Accessed 2026-07-03

Palantir Technologies — Quarterly earnings releases, Q1 2024–Q4 2025 (SEC 8-K filings) — Accessed 2026-07-03