The 61% Blind Spot: Why Your Tax Tech Strategy is Ignoring the CEO

We need to stop building tax as a project and start building it as a product.

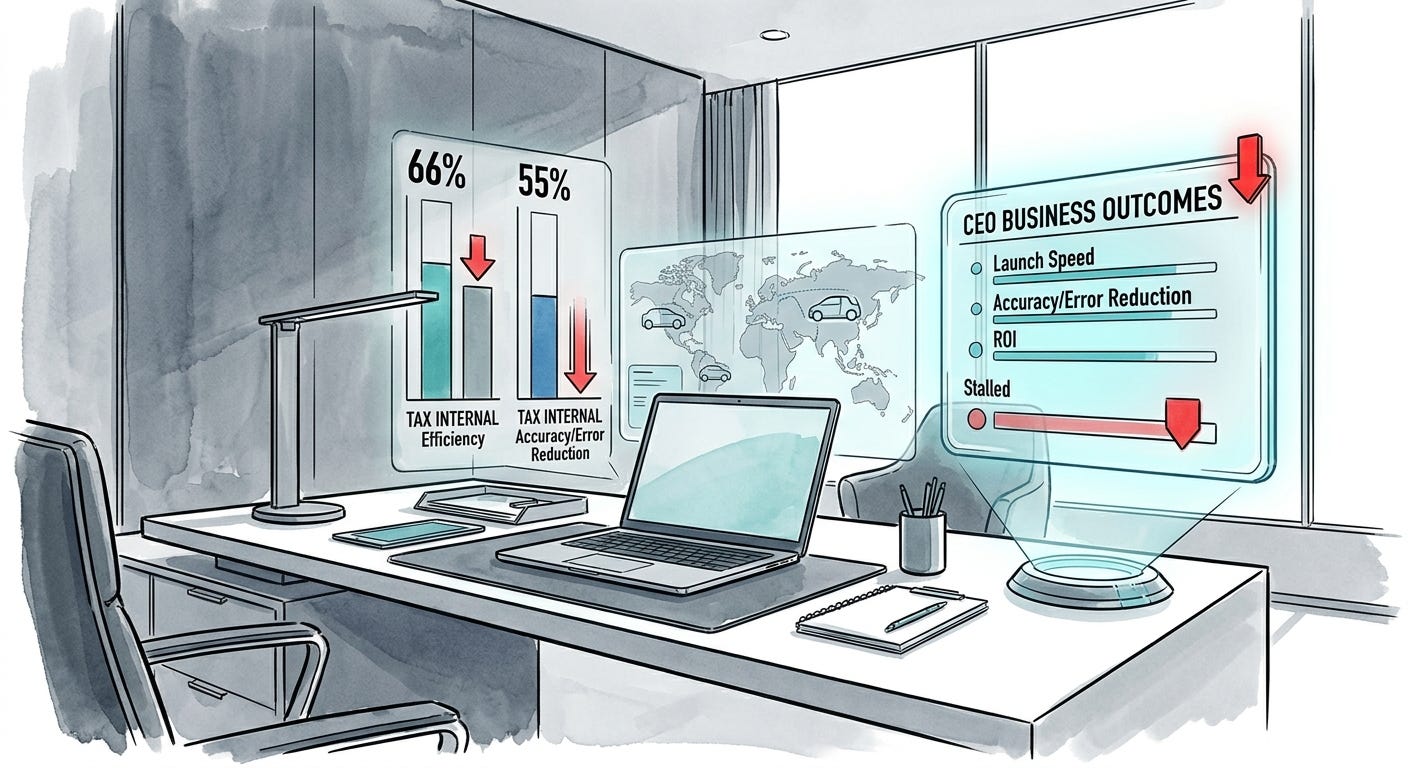

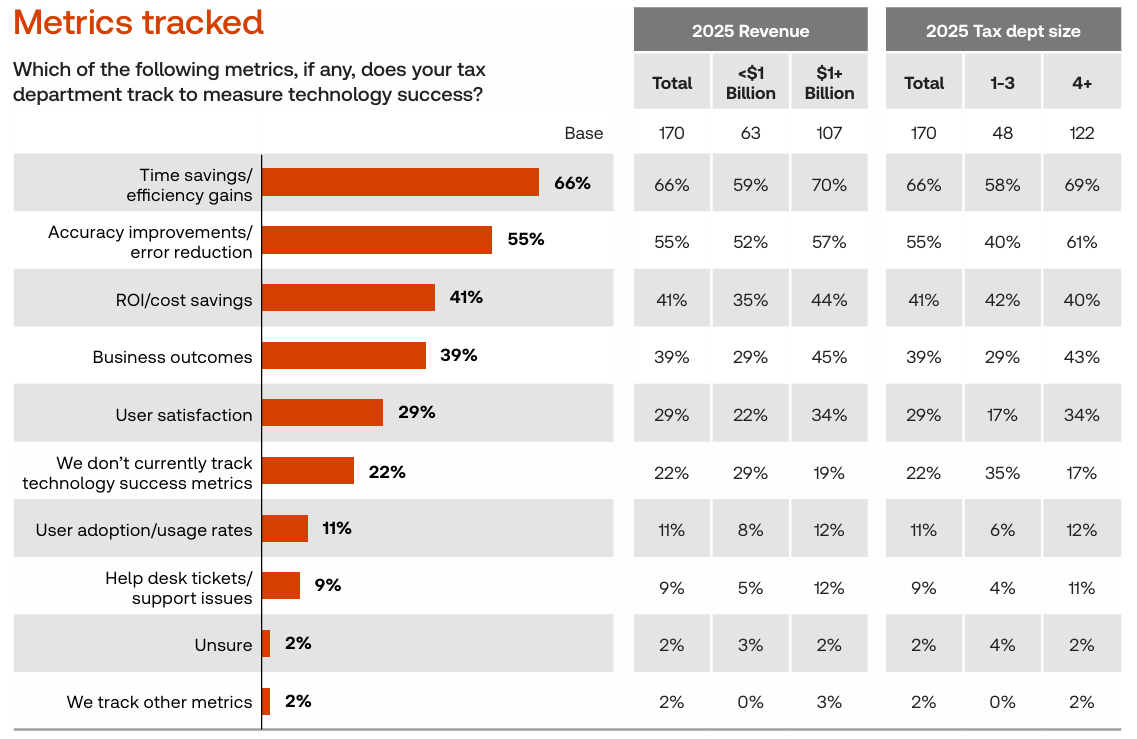

According to the Thomson Reuters Institute’s 2026 Corporate Tax Department Technology Report, 61% of tax departments surveyed are ignoring the only metric that actually matters to the C-suite: business outcomes. Instead, they are still measuring themselves by “Tax Internal” yardsticks. The survey shows they prioritize time savings (66%) and accuracy (55%):

To avoid basing my conclusions on a single report, I had a quick look at what the “Big Four” think about this. The consensus is that measuring “adoption” or “accuracy” alone is no longer sufficient; tax departments must now prove their impact on the enterprise P&L and growth speed.

Main Conclusions:

PwC (AI-Driven Value): Predicts a shift from “ground-up” crowdsourced AI to “top-down” enterprise strategies. Metrics are moving toward “proof points” that link AI-driven tax workflows to market differentiation and P&L impact.

KPMG (Value Driver Trees): Recommends identifying “functional levers” that impact the broader organization, such as optimizing indirect tax cash flow and minimizing irrecoverable taxes to boost working capital.

EY (Controversy & Policy): Focuses on “Tax Risk & Controversy” as a business metric. They suggest that “Time to Resolution” and “Data Readiness for Pillar Two” are critical KPIs to prevent tax from becoming a bottleneck during global expansion.

Deloitte (Resource Mix): Suggests that the “Optimal Resource Mix” (balancing AI, outsourcing, and in-house talent) should be measured by its ability to free up the tax team for “high-value, strategic activities” rather than just cost reduction.

Don’t get me wrong—accuracy is a baseline requirement. It’s the “Compliance Brain” doing its job. But if your tax tech stack only solves for accuracy, you aren’t a strategic partner; you’re an insurance policy.

To move from being a cost center to a value driver, we need the “Product Heart.”

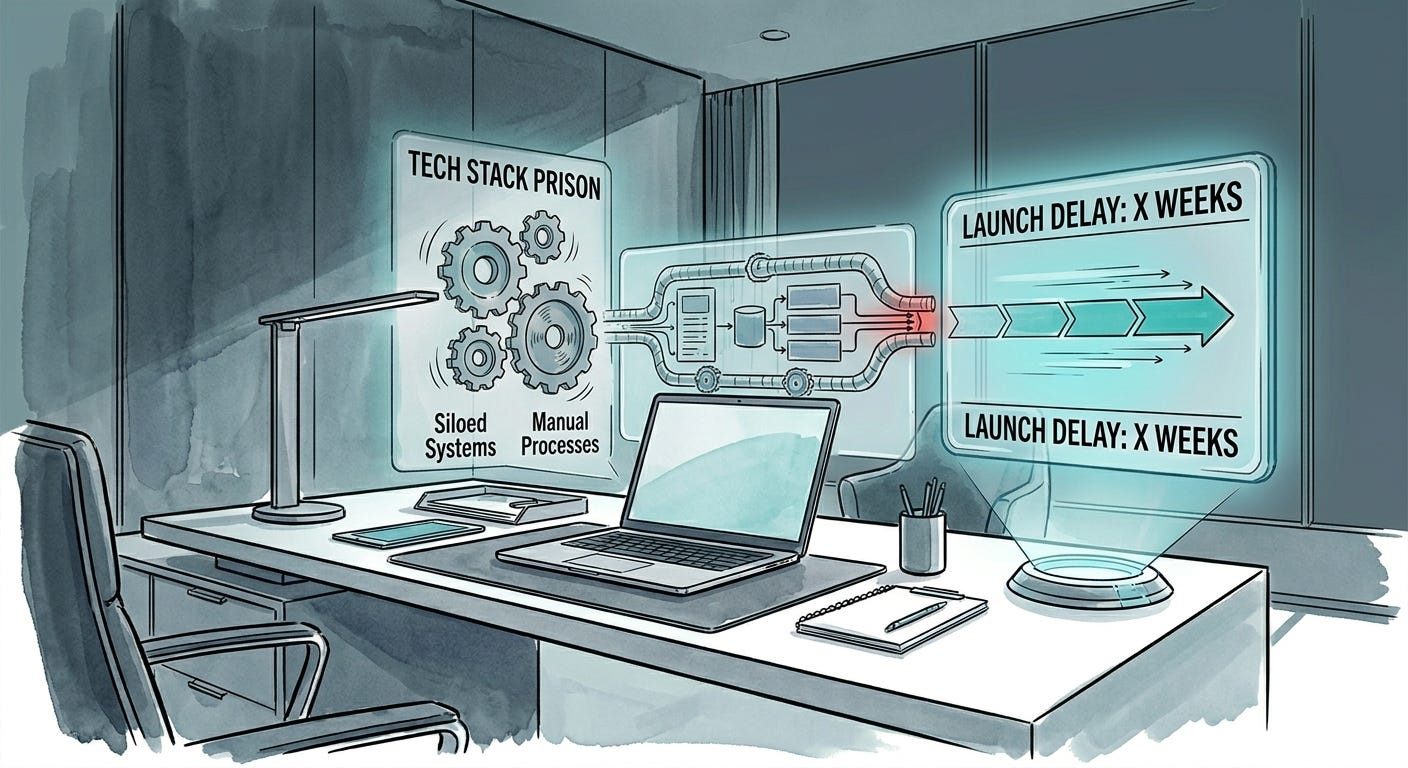

The “Tech Stack Prison” of Internal Metrics

At the S&P 500 scale, “efficiency” is a generic goal. If you save 1,000 hours but your tax logic blocks a new market launch for three months, the net value to the business is negative.

When tax tech is built as a standalone “to-do” list rather than being baked into the product roadmap, it becomes a blocker. We focus on the data trail for the audit we might have in three years, while the business prioritises the checkout completion rate today.

The Pivot: Adopting “Business-First” OKRs

Without a doubt, Tax Departments must bridge the gap between “tax internal” metrics and “business outcomes.” But what can those be?

To align with the “Product Heart” philosophy, these OKRs are categorized by Compliance Hygiene (Efficiency) and Strategic Enablement (Business Outcomes).

Category 1: Business Enablement & Speed (The “Product Heart”)

Objective: Accelerate global expansion and product agility through tax automation.

KR 1: Reduce “Tax-to-Market” Latency (the time to configure tax logic for a new jurisdiction) from X weeks to < 48 hours.

KR 2: Achieve a 0% Tax Latency impact on checkout completion rates by moving tax calculation logic to the “edge” or a real-time engine.

KR 3: Increase the “Tax Incentive Capture Rate” (e.g., R&D credits, OB3 Act benefits) by 15% through automated data extraction.

Category 2: Cash Flow & Financial Performance

Objective: Maximize free cash flow and EBITDA through strategic tax optimization.

KR 4: Increase Free Cash Flow by $X million through real-time VAT/GST recovery automation.

KR 5: Maintain an Effective Tax Rate (ETR) variance of < 1% between forecast and actuals, enabling more predictable capital allocation.

KR 6: Reduce Irrecoverable Tax as a percentage of total spend by X% via improved vendor onboarding logic.

Category 3: Compliance Hygiene & AI Maturity (The “Compliance Brain”)

Objective: Transition to an “agentic” tax operating model to eliminate manual loops.

KR 7: Automate 95% of standard tax reconciliations using AI agents, reducing manual FTE hours by X%.

KR 8: Achieve Audit-Ready Status within 24 hours for any jurisdiction via a centralized “Tax Data Lake.”

KR 9: Maintain a 0% Audit Penalty rate on all “real-time reporting” mandates (e.g., EU e-invoicing).

If you want a seat at the table where the CEO decides on the next $1B investment, your tax tech needs to speak the language of the business.

“We need to stop building tax as a project and start building it as a product. The CEO doesn’t care about the ‘how’ of our reconciliations; they care about the ‘if’ of our global expansion.”

Sources:

2026 Corporate Tax Department Technology Report | Thomson Reuters

Tax changes: A strategic look ahead to 2026 | Thomson Reuters Institute

PwC 2026 AI Business Predictions: Delivering Measurable Outcomes

Deloitte Tax Transformation Trends 2025: Rising to Meet the Moment

PwC Value Creation: Linking Tax Operations to Enterprise Growth