The 2026 AI TaxTech Map: Every Major Partnership YTD

Someone, somewhere, will eventually figure it out.

Every major player in the TaxTech space has an AI strategy. Most have AI platforms. Some have actual results. The competition is now focused on platform procurement (external or internal), adoption by business customers, and results. And it’s getting hot out there.

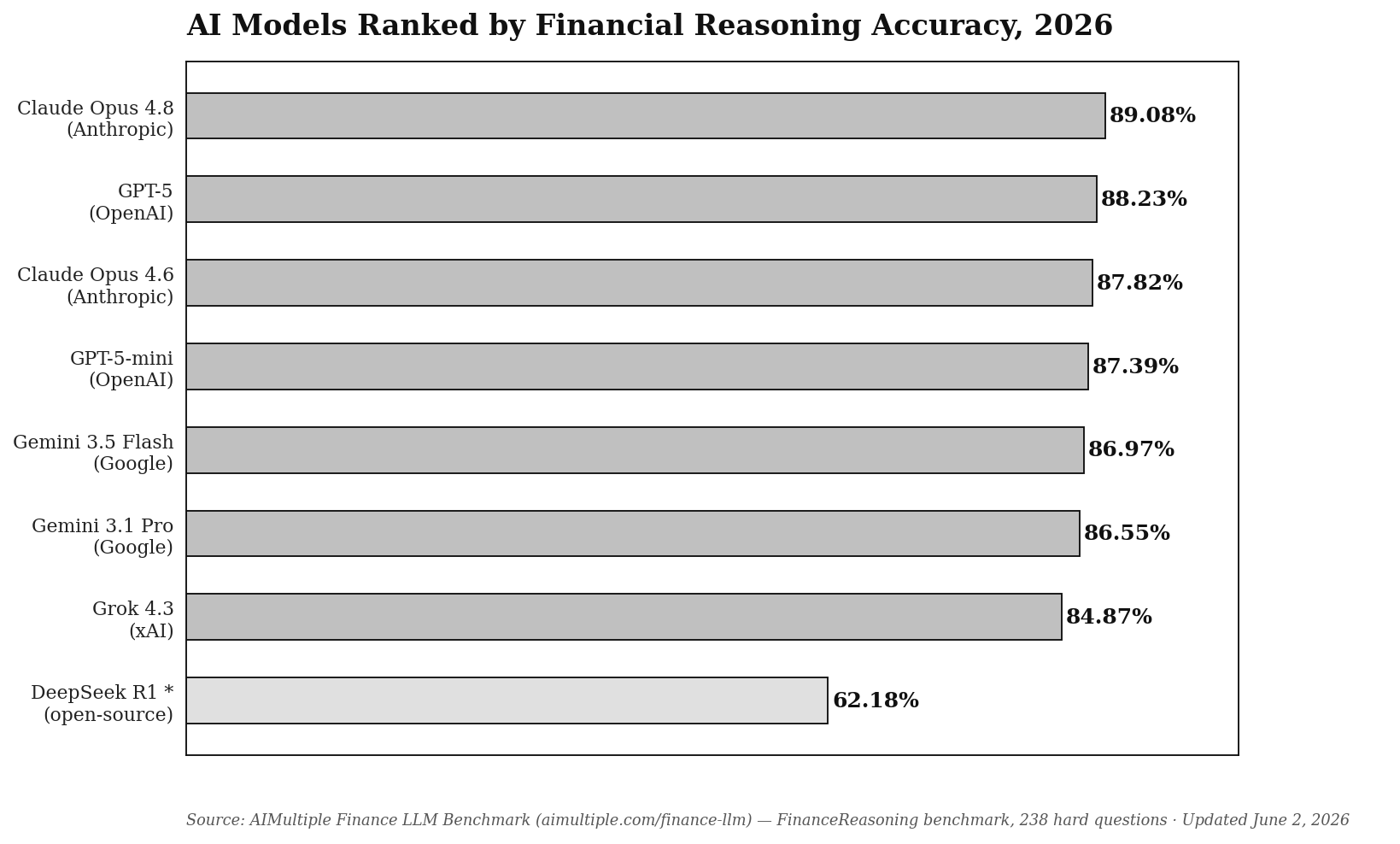

What the Models Can (and Can’t) Do

The AIMultiple Finance LLM Benchmark — 238 hard financial reasoning questions, updated June 2026 — has the clearest current ranking.

Claude Opus 4.8 leads at 89.08%, dethroning GPT-5 (88.23%) while using 7× fewer output tokens. Notably, the top six models are within 2.5 points of each other. Looks like the model choice barely moves the needle at this level. DeepSeek R1 (open-source) trails at 62.18% but is still relevant for European deployments where transaction data can’t leave the infrastructure. It also needs further training to be on par with the rest of the pack.

Clearly, the constraint is not the model.

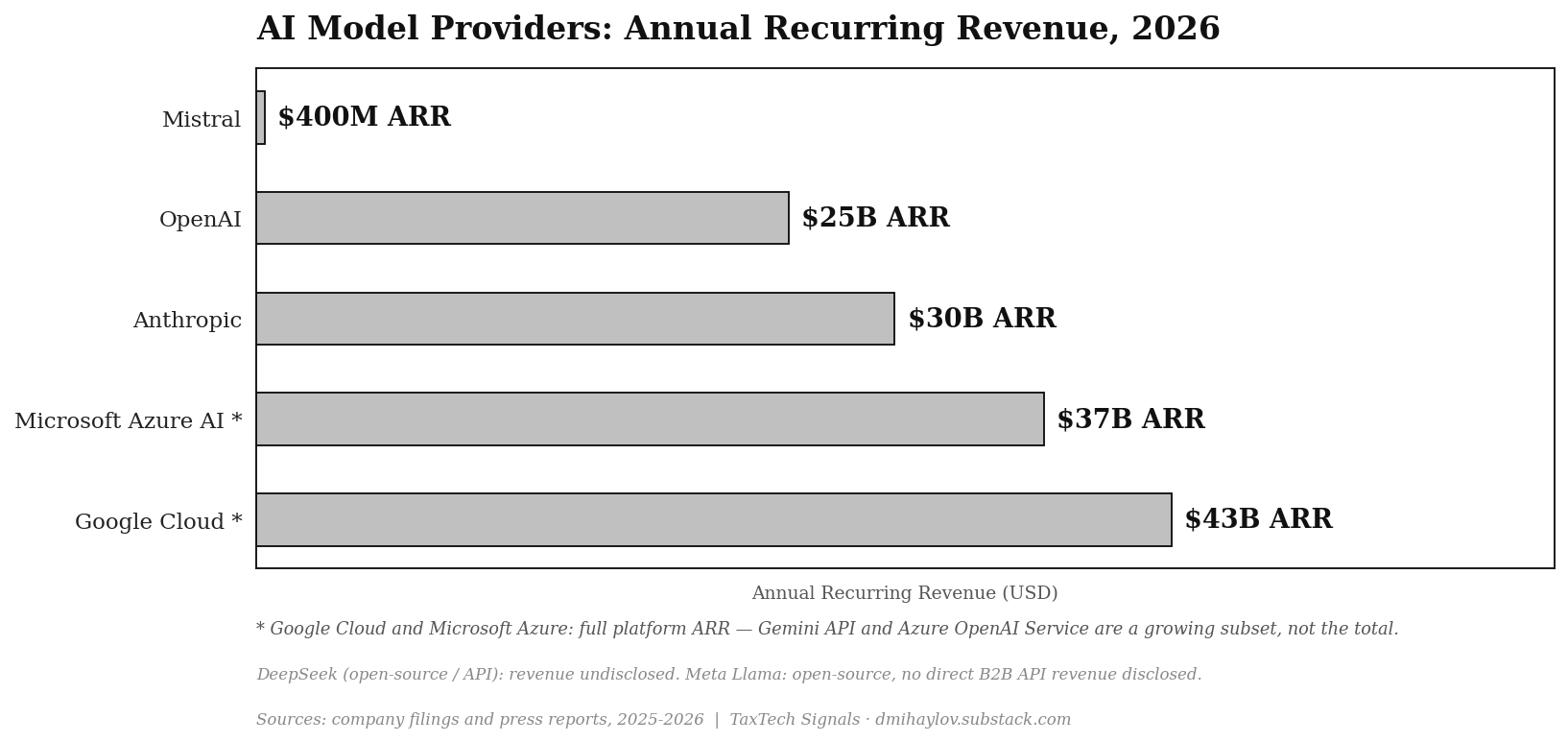

The Providers Building the Infrastructure

Before evaluating any AI vendor, it helps to know who’s funding the underlying models — and how quickly they’re growing.

Anthropic grew from $1B to $30B ARR in 18 months. OpenAI hit $25B ARR — over 40% from enterprise. Mistral crossed $400M ARR through European enterprise deals, 20× in a year.

The interesting dynamic: Anthropic and OpenAI have competing claims on the same enterprise clients. Anthropic signed Deloitte and PwC. OpenAI signed Bain and H&R Block. Both signed Intuit, separately.

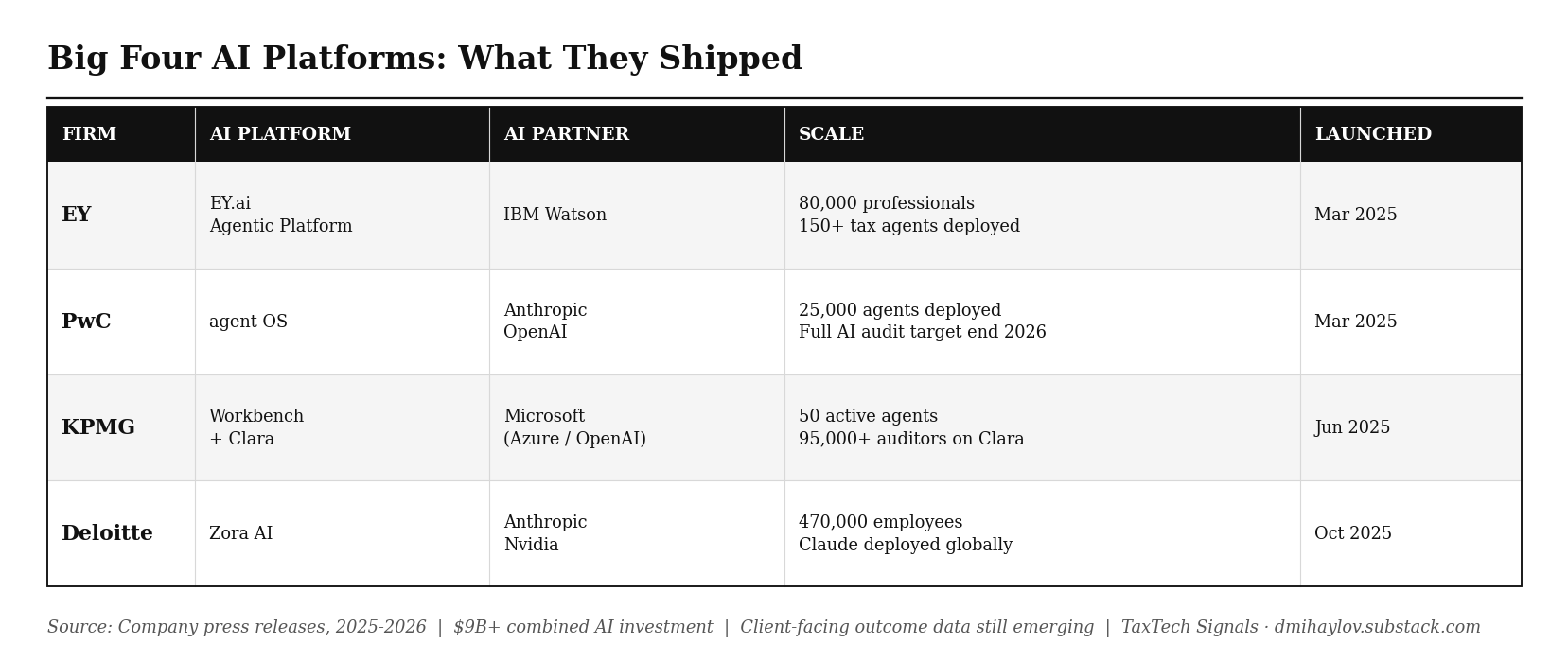

Big Four: $9 Billion and Counting

The combined AI investment across the Big Four is $9B+. Here’s where it went.

The platforms are real. Client-facing outcome data — tax cycle times, audit error rates, jurisdiction efficiency — is still emerging. Whoever publishes that data first and proves fidelity will hold the relationship for the next decade.

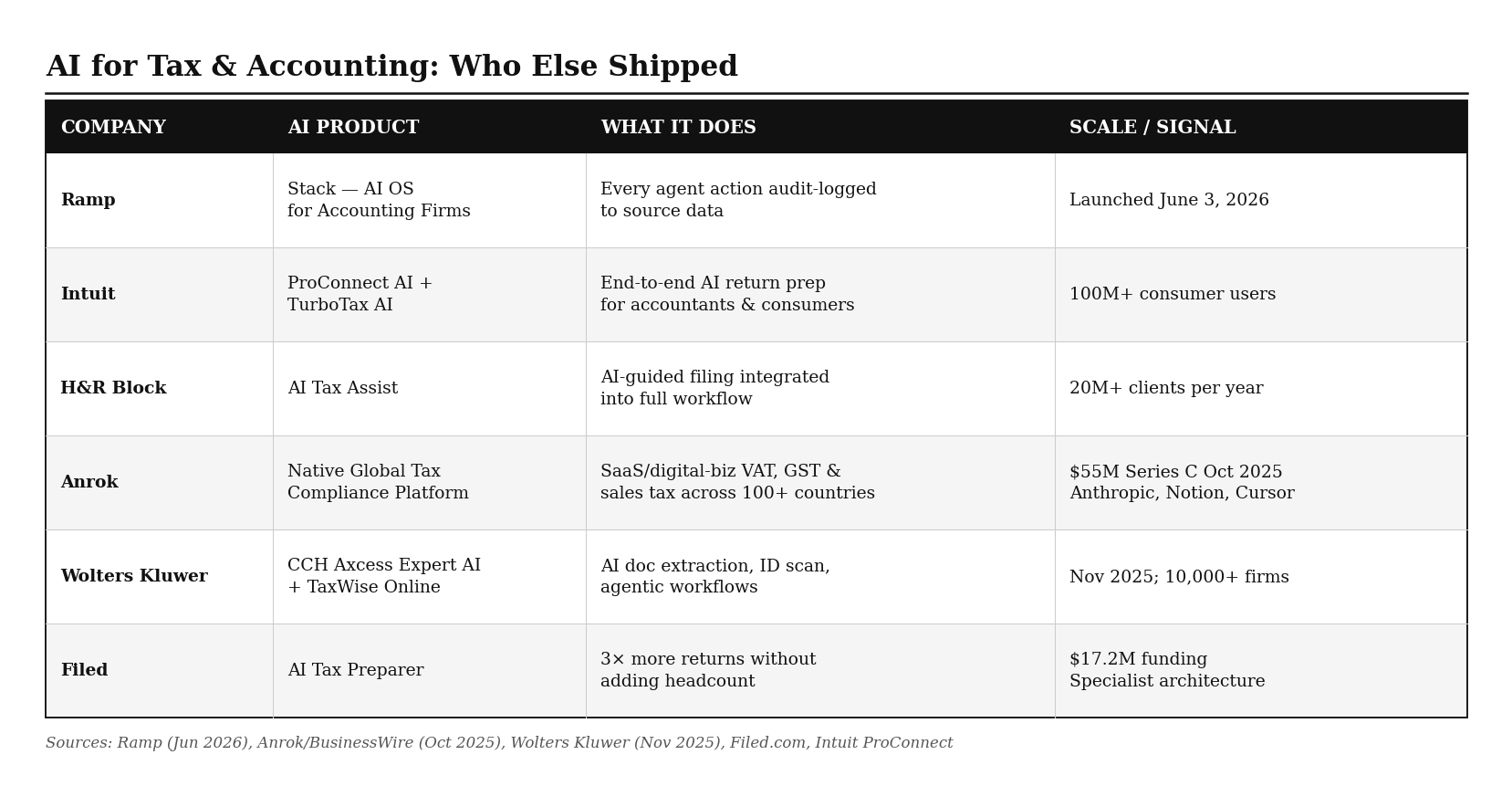

Everyone Else Who Actually Shipped

The more interesting story is happening outside the Big Four.

Ramp’s Stack — a full AI OS for accounting firms, every agent action audit-logged to source data — launched June 3. Anrok raised $55M Series C in October 2025 and now handles VAT, GST, and sales tax for Anthropic, Notion, and Cursor across 100+ countries. Wolters Kluwer shipped Expert AI across CCH Axcess — their unified tax, audit, and firm management platform — in November 2025. Filed built an AI Tax Preparer that processes 3× more returns without adding headcount. A European institution applied LLMs to supplier invoices and achieved a 10% cost reduction on a multibillion-euro spend basis.

79% of tax leaders say AI will be transformational. 37% have invested. Early adopters are getting mixed results. Some will figure it out — and when they do, they’ll have 18 months of hard architecture decisions baked in before the first case study is written. By the time best practice gets published, the advantage is already in the past.

As I argued in Your Tax AI Vendor Cannot Fix This: AI on top of bad data fails quietly. The firms winning right now fixed the data layer first.

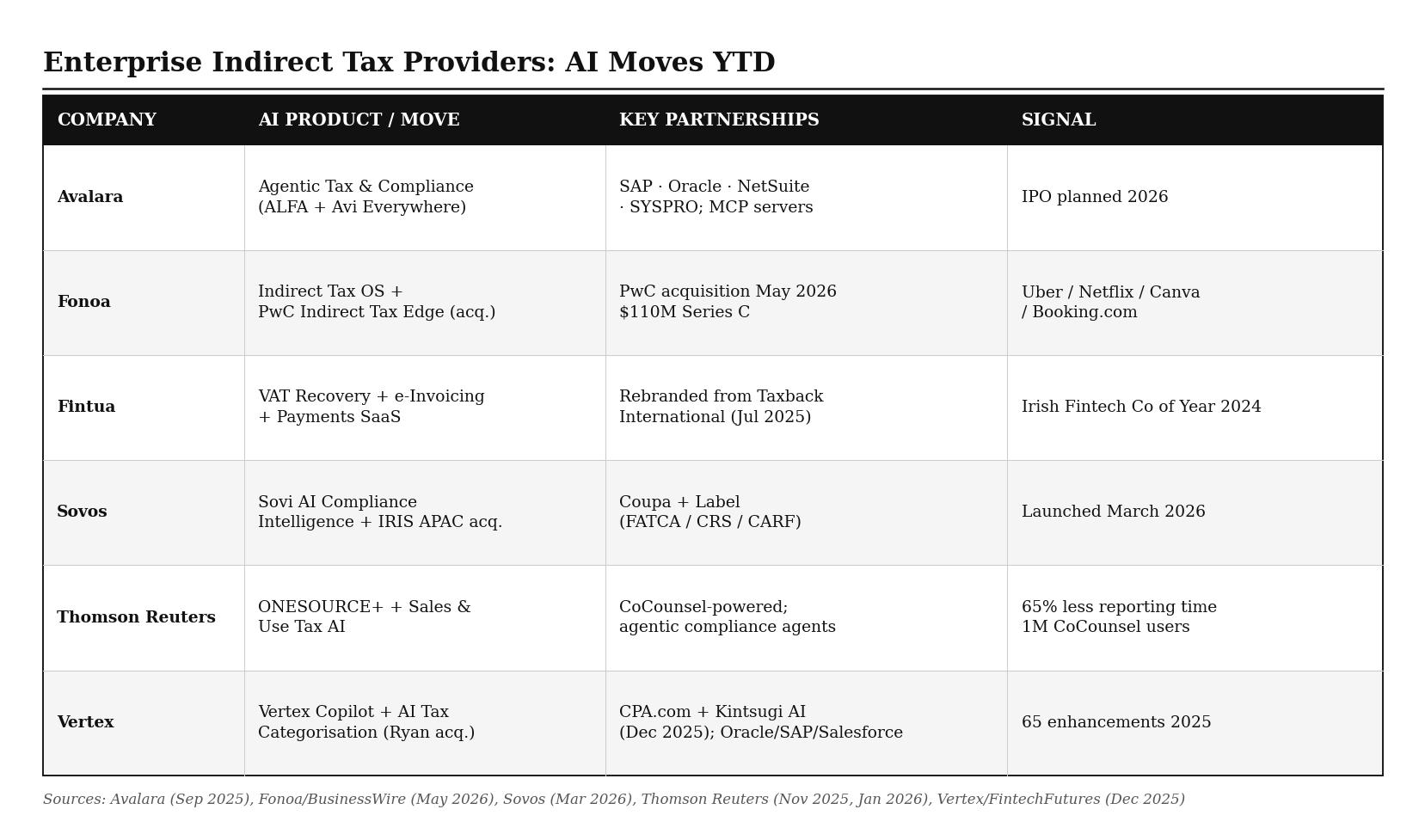

The Indirect Tax Infrastructure Layer

The enterprise indirect tax market — the layer between your ERP and global VAT/GST compliance — is having one of its most active M&A years on record.

Fonoa is the headline story. $110M Series C in May 2026, and they simultaneously acquired PwC’s Indirect Tax Edge platform — the same platform PwC was building to compete with them. They now own both sides of that argument. Current clients include Uber, Netflix, Canva, and Booking.com.

Avalara Launched Agentic Tax & Compliance in September 2025. The ALFA framework enables agents to act autonomously across SAP, Oracle, NetSuite, and SYSPRO — and shipped MCP servers for tool-level integration. An IPO is planned for 2026. The company that defined indirect tax compliance for a generation is now positioning itself as an AI-native orchestration layer.

Sovos Launched Sovi AI in March 2026 and acquired IRIS APAC to expand Asia-Pacific reach. Their Label product handles FATCA, CRS, and CARF. The positioning is deliberate: compliance intelligence as a distinct product category from compliance execution.

Thomson Reuters launched ONESOURCE+ in November 2025 — an AI-powered Intelligent Compliance Network that connects enterprise indirect tax, trade, and risk infrastructure — and then followed with ONESOURCE Sales and Use Tax AI in January 2026. Powered by CoCounsel, it cuts routine reporting time by 65% and audit exposure by 75%. The CoCounsel Tax product already has 1 million users across 107 countries. ONESOURCE is where the indirect tax workflow actually runs — and now it has an AI layer on top.

Vertex acquired AI tax categorization from Ryan in December 2025, added Kintsugi AI the same month, and shipped 65 product enhancements throughout 2025. Vertex Copilot is already embedded in Oracle, SAP, and Salesforce — meaning the AI sits where transactions actually happen.

Fintua — formerly Taxback International — rebranded in July 2025, collapsing VAT recovery, e-invoicing, and payments into a single platform. The rebrand signals compliance as a commodity and automation as the margin.

Every significant player in indirect tax infrastructure either built an AI product, acquired one, or bought a competitor’s platform this year.