Your Tax AI Vendor Cannot Fix This

The gap between what TAs can detect and what your stack can reconstruct is yours to fix. Here's how.

You’ve probably been in the room when your Tax SaaS vendor claimed to have an excellent tax filing audit trail. It lives on their infrastructure. It’s queryable through a UI. You can easily generate and download it. But there’s a catch. It may take 6-8 weeks or more to do it. For one jurisdiction.

I’ve learned this while working on TaxTech infrastructure at Uber. We operate in 70+ countries. Every jurisdiction has different VAT rules, entity registration requirements, and filing cadences. When you’re processing millions of trips, deliveries, and partner transactions per day, the gap between what your transaction system records and what your compliance tool reports can span days, entities, and undocumented transformation steps. Reconstructing how you got there is a different problem entirely — and it’s one the Tax SaaS was never designed to solve. Or at least I have not seen a tool remotely capable of doing this yet.

So, when the IRS, HRMC, or an EU tax authority flags your entity structure or a discrepancy between real-time e-invoicing and VAT reporting, and the inquiry lands, you’ll be facing this very problem. And it’s an issue you’ll face very often because of the sheer efficiency with which tax authority systems can now deploy AI to find even minor inconsistencies in your data.

Last week, I wrote about how three tax authorities deployed AI in 2026 that queries your data rather than your return. The IRS runs Palantir’s SNAP (Selection and Analytic Platform) across 100+ fragmented legacy databases, surfacing entity relationships no human auditor could trace manually. Through a contract with the HMRC, Quantexa is building a Unique Customer Record: a single, consistent view of every taxable entity in the UK, resolved from fragmented public and private sources. The EU AI Act’s high-risk AI enforcement comes into force on 2 August 2026.

The question I left open: how do you prepare for this?

The Readiness Gap, By the Numbers

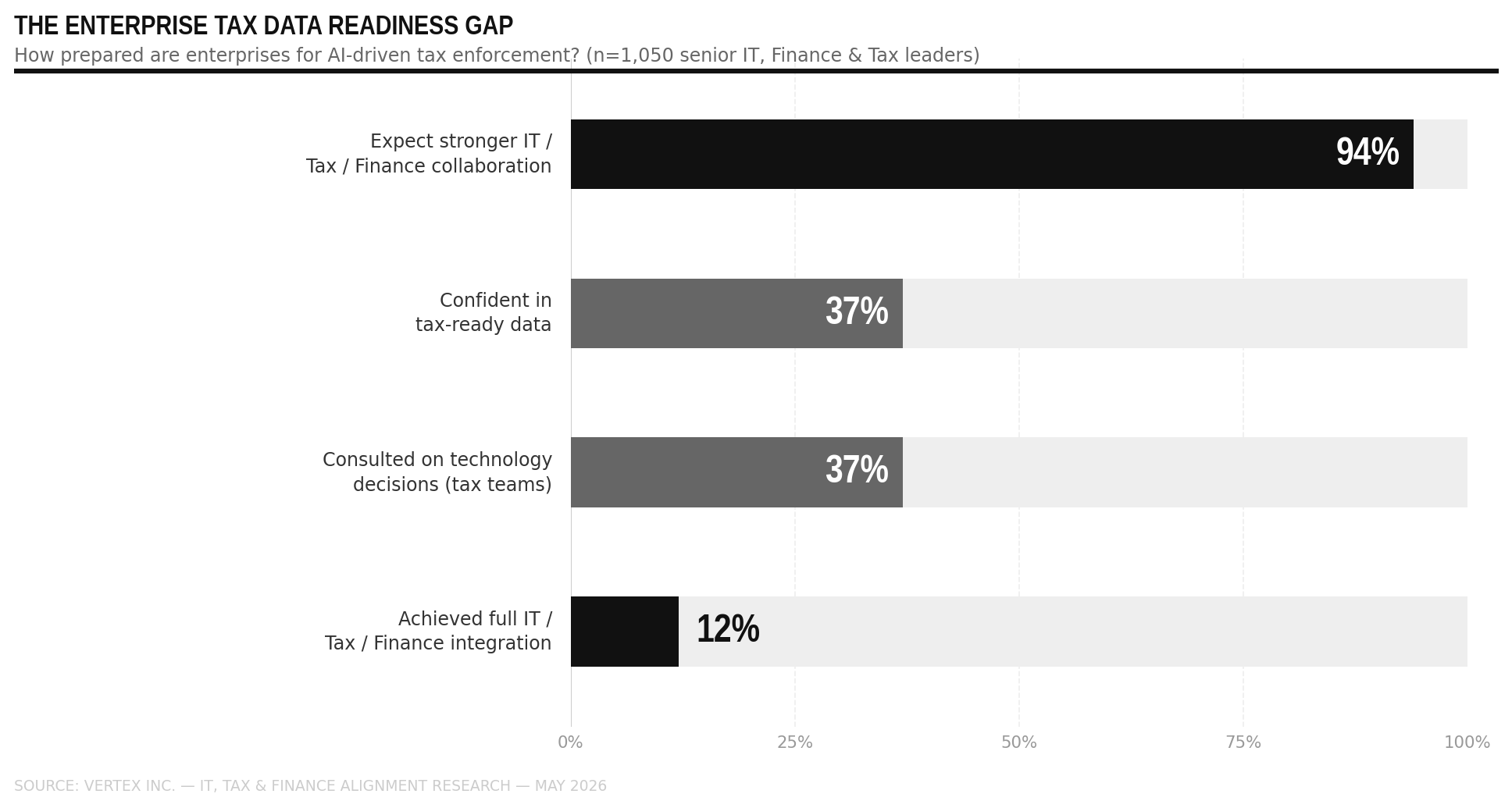

On 19 May 2026, Vertex published a global study of 1,050 senior IT, Finance, and Tax leaders across the US, UK, and Europe:

94% expect stronger collaboration between IT, Tax, and Finance. Only 12% have achieved full integration. Tax teams are consulted on technology decisions 37% of the time. Only 37% report high confidence in their tax-ready data.

I recognize that 12% gap from the inside. At Uber, the product team making decisions about trip pricing, partner fee structures, and payment flows is not the same team filing VAT returns. The decisions upstream create tax obligations downstream — and the pipeline connecting those two realities is something you build intentionally, or you discover under pressure. Most enterprises are discovering it under pressure.

Why Your Vendor Cannot Close This Gap

So, data readiness seems to be the most pertinent compliance risk. The natural move is to buy a tool. I’ve seen it happen repeatedly, and it’s the right call for many problems. But it is the wrong call for this one — for three specific reasons.

1. Your vendor’s audit trail is not your audit trail

When your compliance data lineage lives on a vendor’s infrastructure, you are paying for access to your own operational data. If an inquiry requires you to reconstruct a tax position independently — outside the vendor’s interface, without an active support contract — you discover that the lineage exists only within their system.

At Uber scale, this matters profoundly. What I’ve found is that no single vendor has access to all of our data. Let’s take Portugal as a good example. A trip there touches a local operating entity, a Tax SaaS, a payment processor — each potentially in a different jurisdiction with a different data system. The compliance tool shows the output of that structure, not granular views of the local entity’s ERP, the SaaS vendor’s software, or the payment processor’s dashboard. However, the Tax Authority’s system has a unified view of all data and uses AI to detect discrepancies to the finest detail. So, if you can only explain the output, you’ve already lost the first exchange.

2. The compliance logic lives in a vendor’s black box

In many cases, your vendor provides the tax determination logic—configurable via toggles and rule dropdowns. After all, that’s their bread and butter. But it’s something you don’t actively monitor for correctness, and you cannot explain on demand. A human auditor might accept “it’s a system configuration”. The IRS SNAP and HMRC Quantexa do not. They generate conclusions before the inquiry even arrives. By the time a human asks, the model has already formed a view.

You need to be able to say: here is the rule, here is the source, here is the transformation, here is the timestamp. If the only honest answer is “our vendor configured it,” you’re in trouble.

3. Entity resolution has to reflect your specific corporate structure — not a vendor template.

Vendor entity models are built for the median enterprise. They support a parent holding company, a handful of subsidiaries, and standard related-party taxonomies. They were designed to handle what most companies look like — not what your company actually is.

At Uber, a single trip can touch four legal entities before it produces a VAT-reportable output: the local operating entity that contracts with the driver, the technology licensor that licenses the platform, the payment processor that clears the funds, and the entity that reports the consolidated revenue. Each entity has a different registration, a different role in the intercompany chain, and potentially a different identifier across our data systems. No off-the-shelf entity template maps that structure correctly out of the box. You configure it, you maintain it, and when the structure changes — a new country entity, a restructuring, a merger — you own the update.

HMRC’s Quantexa does not work from your vendor’s entity template. It resolves your structure from Companies House filings, PAYE records, MTD transaction feeds, and cross-referenced VAT registration data — sources your vendor never touches. The result is a Unique Customer Record that HMRC builds from the outside in, using data you submitted to other government systems, not data your vendor configured on your behalf. If that externally resolved view of your entity graph surfaces a parent-subsidiary relationship that your ERP has inconsistently classified across jurisdictions, the algorithm flags it. Your vendor’s template cannot explain the inconsistency because the template was never aware of it.

You own that template, which means it has to be built and maintained by people who understand your corporate structure, not inherited from a vendor taxonomy that was never designed for it.

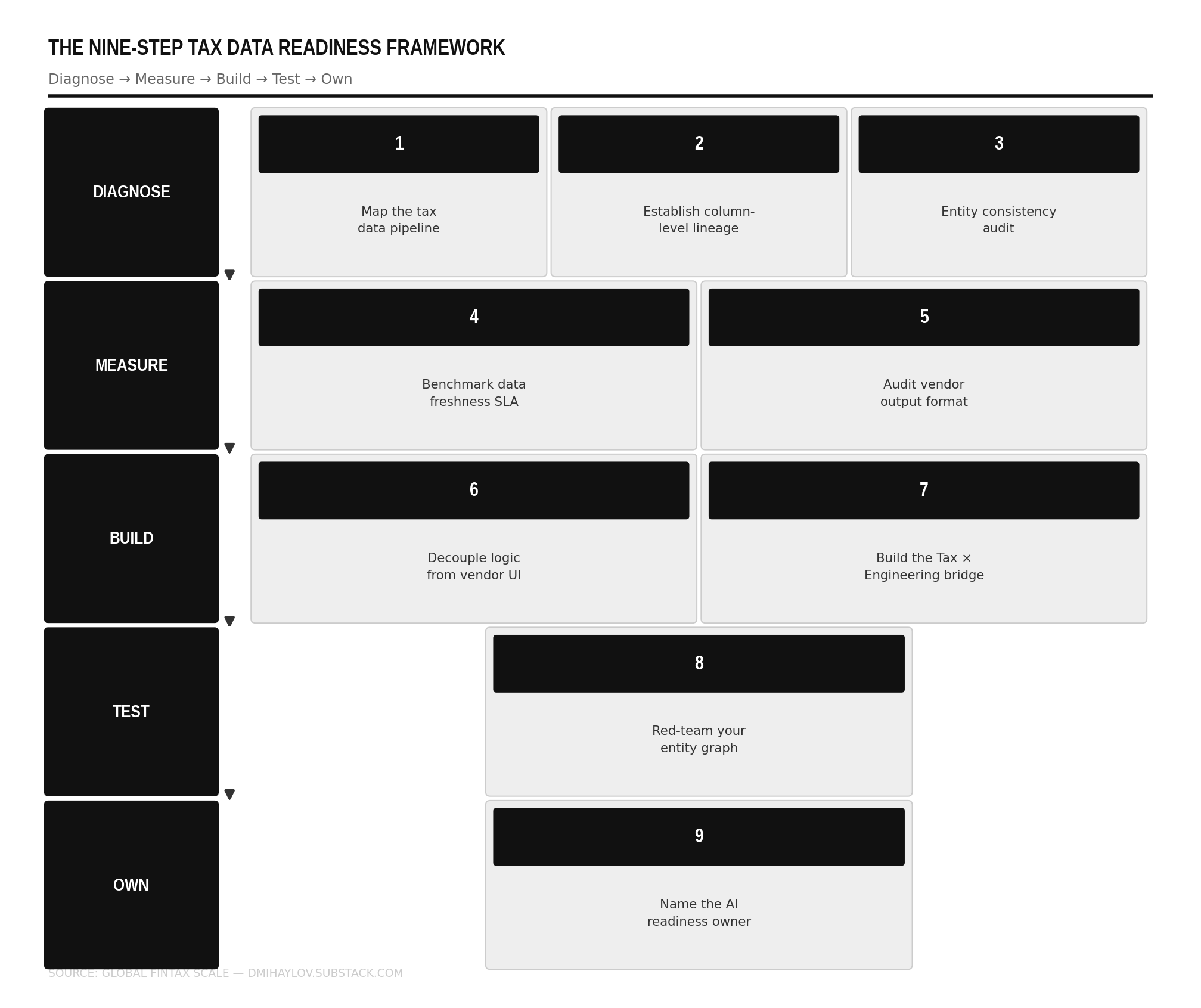

The Nine-Step Enterprise Readiness Guide

These nine steps follow a five-phase arc: Diagnose → Measure → Build → Test → Own. They’re sequenced so each phase builds on the output of the previous one.

1️⃣ Map your tax data pipeline. Find every source feeding a compliance output. Find where the inconsistencies live before the algorithm does.

2️⃣ Establish column-level lineage. For any material tax position: which transaction, which rule, which source, which transformation. If it takes more than an hour to answer, you don’t have defensible lineage.

3️⃣ Run a cross-jurisdiction entity audit. The same entity shouldn’t have different identifiers in your US, UK, and EU systems. HMRC’s Quantexa will find that mismatch. Run it yourself first.

4️⃣ Benchmark your data freshness SLA. HMRC queries real-time patterns against your quarterly filing. If your data is 90 days stale, that gap is your exposure — not your return. Here’s why compliance latency matters.

5️⃣ Audit your vendor’s output format. An ML model cannot query a PDF. If your audit trail is a PDF, it is not an audit trail for an algorithmic adversary.

6️⃣ Decouple your compliance logic from your vendor’s UI. If your vendor is acquired tomorrow, can your engineers independently reproduce the determination logic? If not, version-control it until they can.

7️⃣ Build the Tax × Engineering × Data bridge. Not a committee. A standing function with a charter, a meeting cadence, and a CPO/CTO reporting line.

8️⃣ Red-team your own entity graph. Run the analysis SNAP and Quantexa would run. The IRS AI targets “allocations that don’t match economic reality.” Find those internally before the model does.

9️⃣ Name an owner for AI audit readiness. Not the tax team. Not IT. One cross-functional role, one mandate, one reporting line to the CPO or CTO. If nobody owns it, nobody fixes it.

📥 The full operational guide — with step-by-step instructions, the questions to ask your team, and the tools to use at each phase — is available as a free PDF.

Download: The Nine-Step Tax Data Readiness Guide →

(Free. No paywall. If you find it useful, please share it.)

🔮 Prepare for What’s Coming

By 2028, “tax data observability” will be a defined engineering discipline at S&P 500 companies — with dedicated tooling, named ownership, and SLAs sitting inside Product and Engineering, not the tax function. The CPOs and CTOs who build this infrastructure in 2026 will spend 2028 explaining their methodology to auditors from a position of control. The ones who don’t will spend 2028 reconstructing pipelines under inquiry timelines they don’t control. The gap between those two outcomes is the nine steps above.

Frequently Asked Questions

What data does the IRS AI actually query during a tax enforcement action?

The IRS uses its Selection and Analytic Platform (SNAP), built with Palantir, to query structured transaction data, entity relationships, intercompany flows, and basis records across its fragmented legacy databases. The system compares these against sector benchmarks and historical patterns to flag statistical anomalies — without reviewing a return in the traditional sense. Source: GAO-26-107522, March 2026; Capitol Technology University, 2026; FindLaw.

What is entity resolution, and why does it matter for enterprise tax compliance?

Entity resolution is the process of linking records that refer to the same individual, company, or transaction across multiple databases — even when those records use different identifiers, formats, or naming conventions. HMRC's Quantexa contract is built precisely on this capability. If your enterprise's entity model is inconsistent across jurisdictions, enforcement systems will surface the inconsistency before you can explain it. Source: Quantexa press release; Global Government Finance; The Next Web, May 2026.

How do I make my enterprise tax data audit-defensible?

Audit defensibility requires column-level data lineage: the ability to trace any filed tax position back to its source transaction, through every transformation, with timestamps and ownership records — producible on demand, independently of your compliance vendor, in under one hour for material positions. Manual reconstruction via spreadsheets, email chains, or vendor support tickets does not meet the standard an algorithmic inquiry implies. Source: OvalEdge; JMCO, 2026.

Who should own tax data infrastructure — the tax team, IT, or engineering?

None of them independently. The gap between these three functions is precisely where enterprise tax exposure lives in the agentic enforcement era. A cross-functional role spanning Tax, Product, and Engineering — with a mandate, a budget, and a reporting line to the CPO or CTO — is the correct ownership structure. This is distinct from the tax team, which owns determination logic, and from IT, which owns system availability. Source: Vertex Inc. global research, May 2026.

Should enterprises build or buy their tax compliance technology stack?

Both — but the boundary matters. Vendor tools remain appropriate for commodity compliance tasks: return preparation, statutory filing, and routine determination. Tax data infrastructure — lineage, entity resolution, pipeline architecture, independent audit trail ownership — must be a core internal engineering competency. A vendor can be a layer on top. The pipeline, the lineage, and the ability to reconstruct your position independently cannot be outsourced. Source: Fortune, April 2026; Vertex Inc., May 2026.

I cover the engineering and product decisions that define how enterprises navigate the algorithmic compliance era — one week at a time. If the nine steps above revealed a gap you didn't know you had, subscribe to No BS, Just TaxTech.

REFERENCES & FURTHER READING

Vertex Inc. — “New Vertex Research Highlights Rising Revenue Risk from IT, Tax, and Finance Misalignment” — https://www.vertexinc.com/company/news/latest-news/new-vertex-research-highlights-rising-revenue-risk-it-tax-and-finance-misalignment — Accessed May 2026

Global Government Finance — “HMRC inks £175m deal to boost data, analytics and AI firepower” — https://www.globalgovernmentfinance.com/hmrc-quantexa-entity-resolution-service-data-analytics-ai/ — Accessed May 2026

The Next Web — “HMRC awards £175 million AI contract to British firm Quantexa” — https://thenextweb.com/news/quantexa-hmrc-ai-tax-fraud-sovereignty — Accessed May 2026

Quantexa — “Quantexa Selected by HMRC for Landmark £175M Sovereign Data and AI Transformation” — https://www.quantexa.com/press/quantexa-selected-by-hmrc-for-landmark-pound175m-sovereign-data-and-ai-transformation/ — Accessed May 2026

U.S. GAO — “Artificial Intelligence: IRS Actions Needed to Address Skills Gaps, Information Quality, and Strategic Management” — https://www.gao.gov/products/gao-26-107522 — Accessed May 2026

FindLaw — “IRS Seeking Increased Use of Palantir’s AI and Data Tools to Help Decide Who to Audit” — https://www.findlaw.com/legalblogs/law-and-life/irs-seeking-increased-use-of-palantirs-ai-and-data-tools-to-help-decide-who-to-audit/ — Accessed May 2026

OvalEdge — “Data Lineage Best Practices for 2026: Ensure Accuracy & Compliance” — https://www.ovaledge.com/blog/data-lineage-best-practices — Accessed May 2026

JMCO — “Data Lineage and Audit Trails: What Finance Teams Must Get Right in 2026” — https://www.jmco.com/articles/daniel-shorstein/data-lineage-and-audit-trails-what-finance-teams-must-get-right-in-2026/ — Accessed May 2026

Fortune — “Why your data infrastructure — not your AI model — will determine whether Agentic AI scales” — https://fortune.com/2026/04/30/agentic-ai-data-infrastructure-readiness-scale/ — Accessed April 2026

GoCardless — “Making Tax Digital explained: Your guide to the 2026 Income Tax changes” — https://gocardless.com/blog/mtd-itsa-income-tax-changes-2026-guide/ — Accessed May 2026

Deloitte TaxScape — “Making Tax Digital for Income Tax” — https://taxscape.deloitte.com/article/making-tax-digital-for-income-tax.aspx — Accessed May 2026

PwC — “The next era of tax compliance: real-time and data-driven” — https://www.pwc.com/gx/en/services/tax/connected-tax-compliance/tax-authorities-ai-compliance.html — Accessed May 2026

Capitol Technology University — “Audited by an Algorithm: How the IRS Is Using AI in 2026” — https://www.captechu.edu/blog/audited-algorithm-how-irs-using-ai-2026 — Accessed May 2026

Excellent article, Diddo — but my first thought was around the first of the nine steps, "Map your tax data pipeline. Find every source feeding a compliance output. Find where the inconsistencies live before the algorithm does."

This may be possible at Uber, but it would be completely beyond most large supply chain multinationals with a significant ERP history. Even with AI's help, understanding how that data is stored and maintained in the first place requires more skills than they typically have available.

Even then, the cost-benefit would only make sense if it goes far beyond tax.